Development

·

8

min read

How fintech platforms are built: Design, architecture, and scale

Jan Hauser

Building a fintech platform that survives launch, scales without crumbling and earns lasting customer trust is far more complex than assembling a typical SaaS product.

Drawing on a decade of experience with partners like BankID, Erste and FTMO, we can confidently answer the question “how do you design fintech software?” From navigating the regulatory maze to engineering platforms that scale, here is the field-tested blueprint for founders, product leaders, and engineers stepping into the space.

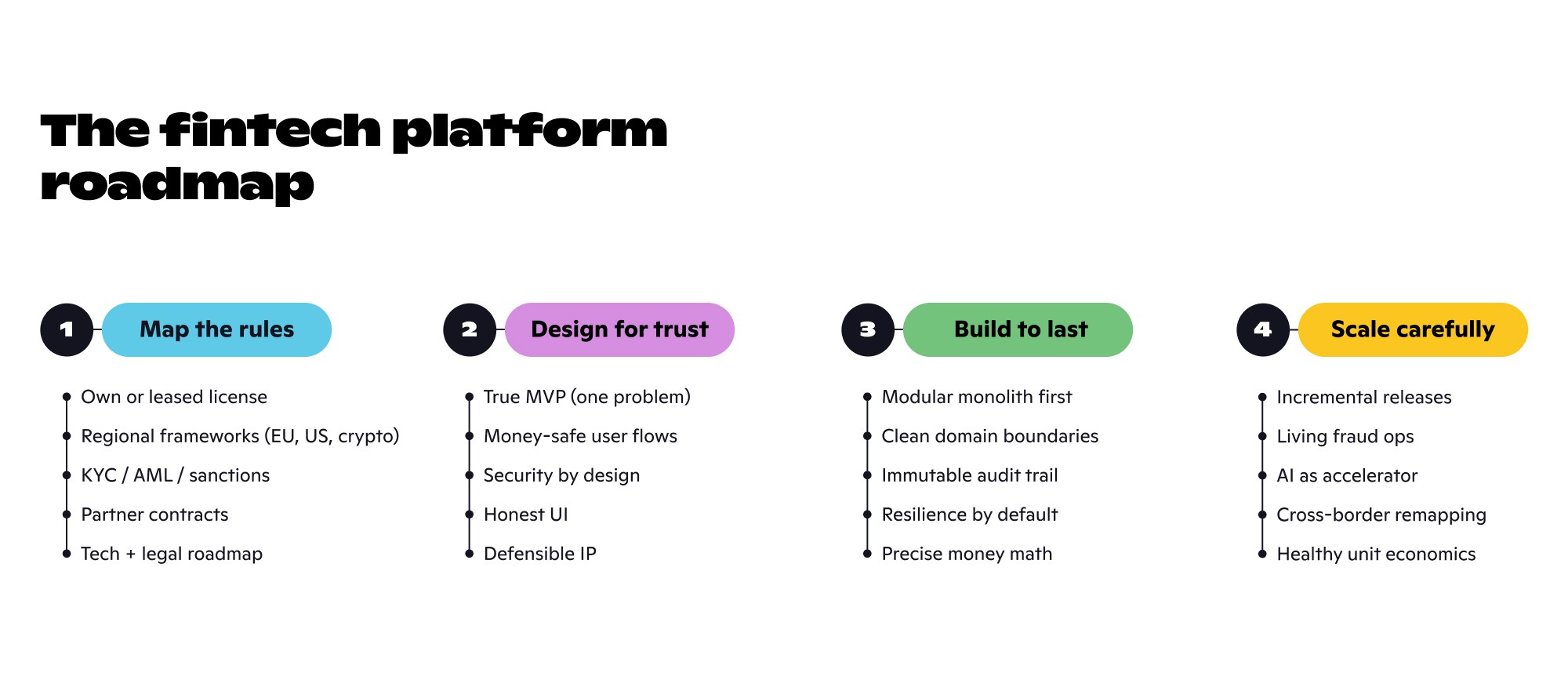

The fintech development process

Most software projects begin with a feature wishlist. The development process for a fintech platform begins with a regulatory map. Before a single line of code is written, you must map the regulatory environment in every target jurisdiction.

Do you need your own license, or will you partner with a platform that leases you theirs as an enabler?

Even if you lease, plan your path to independence. Not having a full regulatory roadmap can block you from onboarding customers later, choking revenue, MRR and ARR overnight. Compliance is a direct growth lever.

What regulations apply to fintech apps and software?

They’re extensive and regional:

In Europe and the UK, PSD2/PSD3, Open Banking and Open Finance regulations set the table. You’ll deal with KYC/AML directives, GDPR, safeguarding requirements, consumer duty, and PCI DSS if you touch cards.

In the US, it’s a state-by-state patchwork plus federal oversight from the CFPB, FinCEN and others.

Dealing with crypto? Add MiCA, Travel Rule and evolving guidance.

Every regulation has technical implications, including:

Audit trails

Data residency

Identity verification

Transaction monitoring

Fraud scoring

Sanctions screening

Consent management

These are not features you bolt on later—they are architectural pillars you design around.

Once the regulatory landscape is clear, the development process continues with a true MVP, minimally defined around the one problem that makes your solution unique. Feature lists are infinite. Your first launch isn’t. Pair that with:

Tech roadmap that maps regulatory requirements into technical milestones

Legal roadmap that accounts for Terms & Conditions, customer agreements, data processing agreements and partnership contracts with banks, PSPs and processors.

Those contracts often consume more calendar time than writing the code itself.

Fintech app validation and IP

Market research before code is non-negotiable. Product validation, quantitative and qualitative research, competitive advantage mapping, and a clear path to breakeven form the foundation of your bulletproof plan. If you feel unclear in any area, investors and customers will expose it. Bounce your plan off advisors, build a thick skin and iterate on paper—it’s drastically cheaper than refactoring a product nobody wants.

Now more than ever, defensibility matters. AI-accelerated software development has dramatically lowered the barrier to shipping a fintech product, and the market is more crowded than ever.

Some claim “SaaS is dead.” We disagree, but the bar has risen.

Your intellectual property and the team you build around it become the moat.

Whether it’s proprietary risk models, unique data assets, or deep workflow integrations, double down on IP from day one. Everything else can be replicated—your unique problem-solving engine cannot.

How do you design fintech software? The UX/UI and architecture intersection

Designing fintech software is an exercise in tension. You're moving real money—the interface has to feel safe while staying fast enough to compete with the consumer apps your users already love.

Customers today are extremely demanding about seamless UX/UI. A clunky onboarding flow or a confusing transaction history erodes trust in your ability to handle money safely.

But fintech design goes deeper than screens. The real question, “how do you design fintech software?” lives at the intersection of user experience and system architecture.

Start with an in-depth tech analysis and parallel UX/UI design. Map user journeys that involve moving money, reconciliation, settlement timelines, chargebacks, disputes, and make sure your UI doesn’t lie about what’s happening under the hood. This is where junior teams burn months they didn’t budget for. Treat it as a first-class design constraint, not an afterthought.

Fintech is security-heavy, and if you don’t build around robust encryption, secure data handling and resilient access controls from day one, you’ve already lost user trust.

Security requirements cannot be omitted. Design them like they're permanent, because they effectively are. When possible, use secure third-party data storage partners rather than mirroring sensitive data in your own environment early on (unless your compliance framework permits it).

Development architecture: From modular monolith to scale

The term development architecture is often mistaken for microservices from day zero. That’s a trap.

Start with a modular monolith. Isolate domains (users, accounts, payments, compliance) within a single deployable, but logically separate them with clear boundaries. This gives you the speed of a monolith and the upgrade path to services when true scale demands it.

Equally critical are visibility, traceability and monitoring. These are not optional observability buzzwords.

In fintech, you need to know exactly what every transaction is doing, where it got stuck and who touched it.

You’re building evidence, because regulators and auditors will ask. Your architecture must generate an immutable, queryable audit trail with defined retention periods. Plan your data strategy with the regulator in mind from the start. There’s no AI product enhancement without the right data foundation and no compliance pass without proof.

Resilience comes next. Define uptime SLAs, build disaster recovery plans and design for graceful degradation. Money movement platforms don’t have the luxury of best effort availability. Your development architecture must treat failures as normal, especially when orchestrating across multiple third-party PSPs, processors and banking partners.

Handling financial figures? Make absolutely sure the decimal point is in the right place and that you’re using appropriate numerical data structures. A floating-point rounding error is a regulatory and reputational incident.

Fintech software development execution: Teams, tools, and trade-offs

When it’s time for fintech software development, your team composition dictates success. Do you have in-house deep tech capability? Build on your own. Prefer to stay hands-off? Find a trusted software partner with fintech domain expertise. Have a technical product owner and some engineering muscle, but not enough capacity? Go hybrid. Be realistic that a new team needs time to hit the right velocity.

AI is a powerful accelerator, but it’s not a silver bullet.

Use AI tools to speed up boilerplate, testing and documentation, but keep them under the control of engineers who understand both the code and the financial domain. Vibe coding won’t produce a robust, compliant fintech platform.

Multi-role, AI-accelerated professionals are already on the market—designers who think in product specs, product managers who run their own tech analysis, engineers who can architect the systems they build. Hire them. They’ll connect dots that single-role hires cannot.

Also, treat KYC/AML and fraud systems as living, breathing operations. Real-time monitoring, fraud scoring, sanctions screening—these aren't "set it and forget it" systems. They need ongoing tuning by people who watch the false-positive rate as closely as the catch rate.

Get the balance wrong, and you either bleed through fraud or shed legitimate customers at checkout. Treat them as product features that require iteration, not static compliance checkboxes.

The scaling journey: Why expansion is always slower than you think

Scaling a fintech platform is a never-ending journey. A 3-month build cycle doesn’t finish it. Bugs surface. Gaps appear. Customers tell you things you didn't want to hear, and reshape your roadmap. Adopt incremental builds, maintain a transparent release plan and reflect customer wishes strategically, not all of them, but enough to build value worth paying for.

Expansion plans hit walls that aren’t just about capital. Regulatory environments differ from region to region. Adding a new country means remapping compliance, onboarding new PSPs or card issuers, and adapting your product to local payment methods and data-residency rules. Due diligence and technical onboarding with payment partners take significant calendar time—plan these timelines early and align them with your market entry ambitions.

In Europe and the UK, Open Banking and Open Finance regulations are tremendous enablers.

They lower the barrier to accessing account data and initiating payments, but using them requires architectural commitment to consent management and API integrations built on strict standards. Treat these rails as accelerators, not afterthoughts.

Marketing for a B2C fintech product is the key consumption line of your budget, often outpacing technology spend. Factor it in from day one. Customer acquisition cost, lifetime value and operational overhead all sit alongside your tech investment. Fintech is tech-heavy, but it’s also a unit economics business.

The fintech advantage and final trade-offs

Yes, fintech is hard. But it’s also uniquely enabling. The rise of BaaS (Banking-as-a-Service), embedded finance, and licensed enabler platforms means you can launch with a fraction of the overhead required a decade ago.

Focus fiercely on your IP, lean on SaaS for the rest initially and don’t reinvent the money-movement plumbing until your volume demands it.

The most successful fintech products today don’t necessarily charge customers directly; they offer value-added services on existing rails and profit from efficiency gains, low friction and high value. They treat regulation as a product input, architecture as a scaling enabler and their development process as a disciplined blend of risk management and rapid learning.

Building a fintech platform is a marathon.

The teams that scale don't move faster than everyone else—they move more carefully. They treat regulation as a product input from day one. They design for the audit they haven't had yet. They build the team to match the system, not the other way around. None of this is glamorous, but it's what separates a platform that compounds from one that buckles under its own compliance debt.

Got a fintech platform on the roadmap? Talk to the team that's built one.